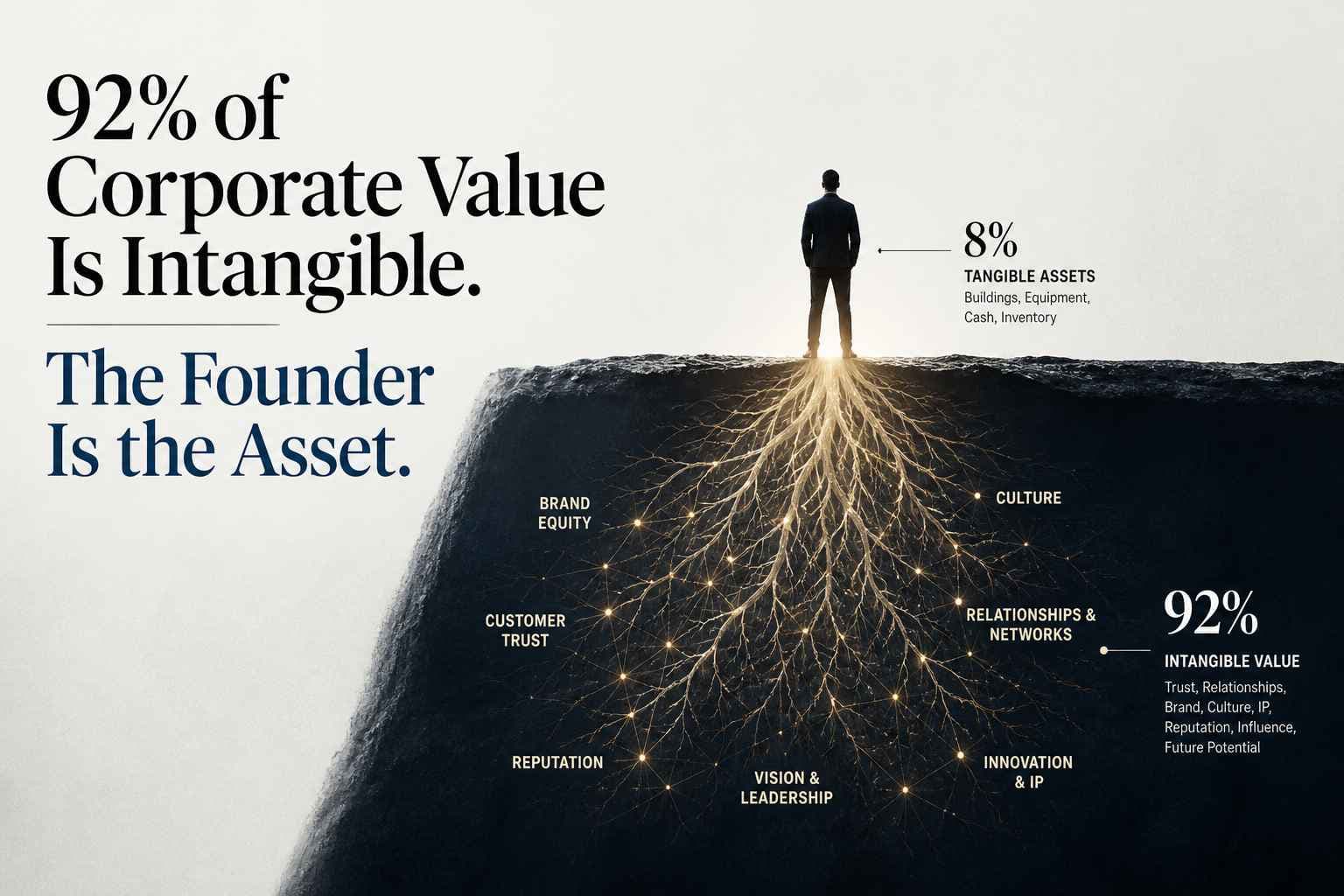

AJ Kumar argues the most mispriced line on the modern balance sheet is the founder. Reputation, judgment, and stakeholder confidence concentrate in the person at the top, not in the trademark or the PR function.

Key Takeaways

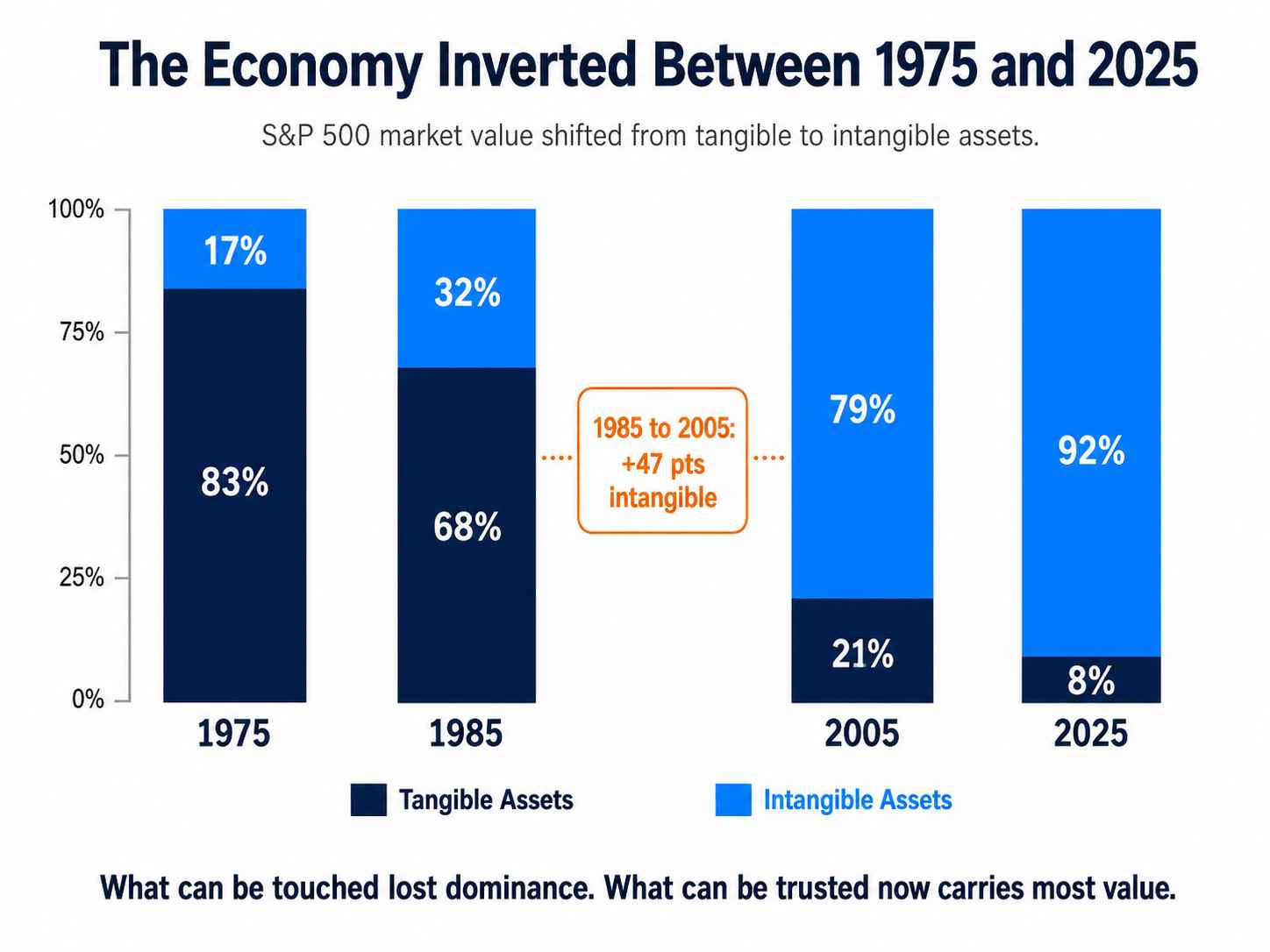

Ocean Tomo data shows tangible assets fell from 83 percent of S&P 500 market value in 1975 to 8 percent by 2025

Burson Reputation Capital research priced reputation at $7.07 trillion globally and 4.78 percent in unexpected annual shareholder return

Intangible asset market value surged from 32 percent to 79 percent between 1985 and 2005, a 47 point swing in two decades

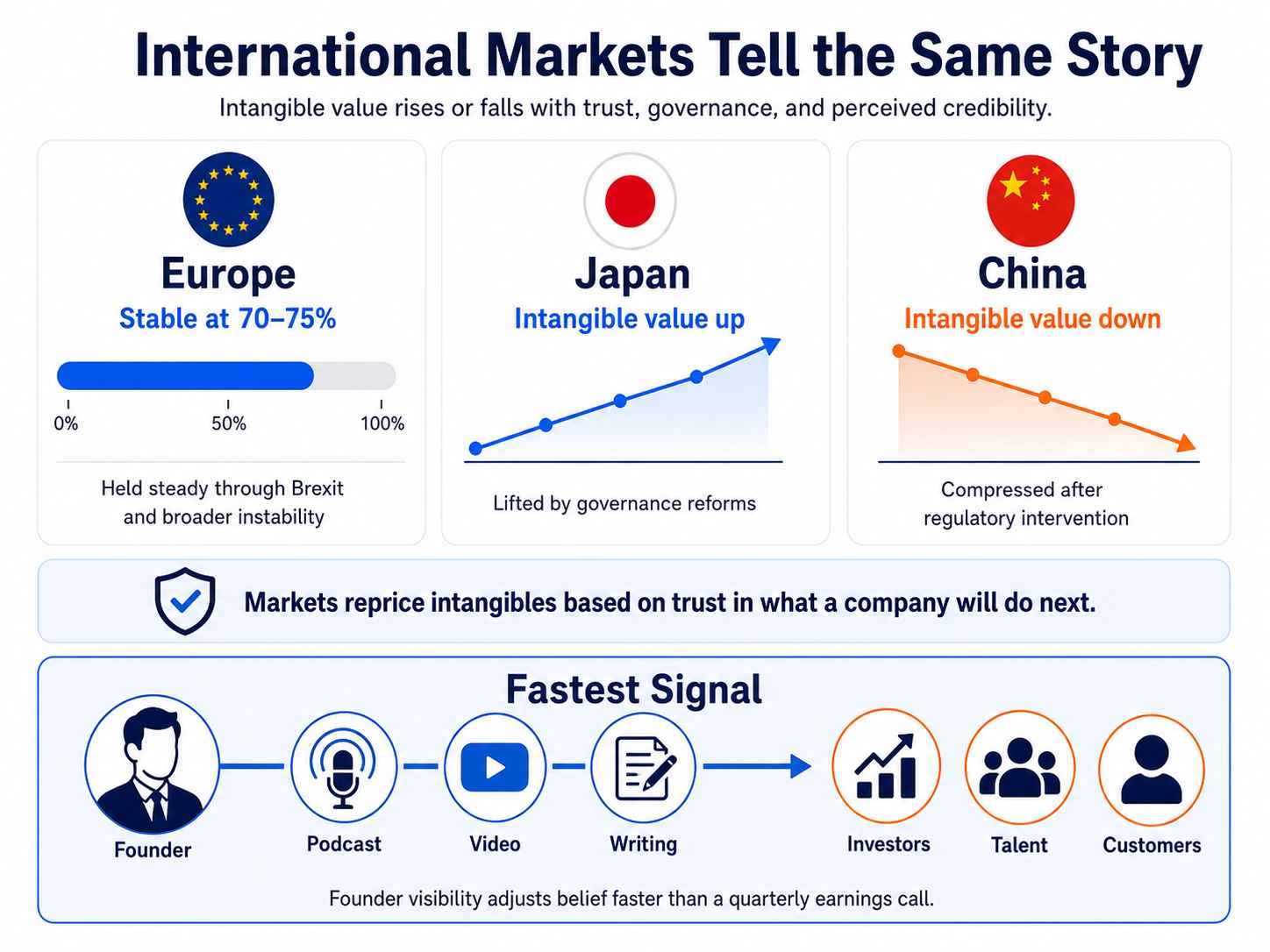

The S&P Europe 350 has held intangible asset levels at 70 to 75 percent through geopolitical and regulatory volatility

China's CSI 300 saw intangible value decline after regulatory crackdowns, proving institutional credibility is a financial input

Founder visibility is the highest-leverage intangible asset because reputation concentrates in a person, not a trademark

The Economy Inverted Between 1975 and 2025

Tangible assets owned 83 percent of S&P 500 market value in 1975. By 2025 they owned 8 percent. The Ocean Tomo Intangible Asset Market Value Study tracks this 50-year inversion. The U.S. data covers half a century. International data covers 20 years. What can be touched lost three quarters of its weight on the balance sheet. What can only be thought, perceived, and trusted now carries 92 percent.

The shift has a cliff inside it. Between 1985 and 2005, intangible market value moved from 32 percent to 79 percent. A 47 point swing in two decades. The Industrial Revolution took a century to restructure the economy. The intangible revolution did the same work in a single working career.

Most boardrooms still allocate attention as if the chart never changed. Buildings, inventory, and equipment get full audit cycles. Reputation, judgment, and founder visibility get a quarterly LinkedIn calendar review. The scoreboard moved. The governance did not.

Reputation Just Got Repriced at $7 Trillion

Burson's 2026 Global Reputation Economy report quantified the asset class directly. Across 66 publicly traded companies, reputation contributed an average 4.78 percent in unexpected annual shareholder return. Scaled globally, that translates to $7.07 trillion of stock market value driven by stakeholder perception, not fundamentals.

The methodology was validated by Dr. Felipe Thomaz at the University of Oxford's Saïd Business School.

Burson identifies eight levers behind reputation. Four performance levers: products, innovation, financial performance, creativity. Four foundational levers: leadership, governance, workplace, citizenship.

Top quartile companies outperform the bottom quartile by 11 to 15 points across every lever. The biggest gaps appear in innovation, product delivery, and governance.

Reputation is now measurable. That move alone changes the conversation. A line item that boards used to file under "soft" sits next to revenue, EBITDA, and growth rate. The question is who controls it.

The Comms Industry Wants to Own This Asset. The Founder Already Does.

The comms industry read the same data and made a positioning move. The Public Relations and Communications Association published a new definition in 2026. PR is now framed as a strategic management discipline that builds trust and enhances reputation. Translation: PR should sit at the management table because intangibles dominate enterprise value.

I do not buy the protagonist. PR is a function. The asset is a person. Stakeholder perception does not concentrate in a department, a press release, or a brand guideline. It concentrates in the founder whose judgment, voice, and conviction become the company's perceived authority over time.

This is not a knock on comms teams. They are downstream of the asset. The Wadds analysis is correct that reputation is now financial. The mistake is assigning the asset to the function that distributes it instead of the person who creates it. A founder with no public presence cannot be packaged into trust by a stronger agency. A founder with conviction and visibility produces trust the agency only has to amplify.

What the Trademark Cannot Hold That the Founder Can

A trademark cannot demonstrate judgment under pressure. It cannot answer hard questions on a podcast. It cannot hold a perspective on the future of an industry. It cannot age, evolve, or change its mind. The corporate brand was built to serve a tangible-heavy economy. What mattered then was machines, inventory, and distribution. Logos signaled stability. The era rewarded the abstraction.

The intangible economy rewards the opposite. Investors do not buy logos. Acquirers do not pay multiples for typography. Top talent does not relocate for a brand voice document. Every high-leverage stakeholder is reading the founder's mind through every public surface available. They price the company off what they find.

I write about this in GURU, INC. through a framework I call the Brand Moat. It has four elements: owned distribution, category association, ecosystem depth, and compounding returns. A trademark cannot build any of the four on its own. A founder with a personal brand moat builds all four at once. The asset is portable, contextual, and human.

International Markets Tell the Same Story With Different Accents

The S&P Europe 350 has held intangible asset levels at 70 to 75 percent. That stability persisted through Brexit, regulatory reform, and broader geopolitical instability. Japan saw a material uplift in intangible value after corporate governance reforms. China's CSI 300 moved the other direction. Intangible asset value declined sharply after regulatory intervention in technology and education sectors.

The pattern is structural. Markets reprice intangibles based on perceived trust, not only disclosed earnings. When governance signals improve, intangibles rise. When institutional credibility takes a hit, intangibles compress. The variable is not what the company does. It is what stakeholders believe the company will do next.

Founder visibility is the most efficient mechanism for adjusting that belief deliberately. A quarterly earnings call reaches one audience on one schedule. A founder publishing across podcasts, video, and writing reaches investors, talent, and customers in the same week. The authority signal is wider, faster, and harder to misinterpret.

The Three Boardroom Mistakes That Misprice the Asset

Boards still treat the founder's public presence as marketing, content, or PR. All three are downstream functions. None of them describe what the founder owns.

Mistake one is measuring impressions. A reach number in a marketing dashboard tells you nothing about how the next acquirer frames your multiple. Mistake two is outsourcing voice to a comms team. The asset compresses the moment a ghostwriter speaks louder than the founder.

Mistake three is treating visibility as optional. In an intangible economy, silence is not neutrality. It is a discount the market applies to anything it cannot interpret.

Founders who internalize the inversion stop measuring the wrong thing. They stop asking what their content produced last quarter. They start asking a sharper question.

Which acquirer, investor, or executive hire is more likely to back them next quarter? The advantage goes to the founder whose thinking they have already encountered. Alex Hormozi sold 2.9 million books in 24 hours. The launch worked because his presence was already the asset.

The Personal Media Company Is the Asset Structure

A founder cannot own an intangible asset without a structure that creates and compounds it. I call that structure the Personal Media Company. It has five components: programming, distribution, monetization, operations, and measurement. They run as one system instead of five disconnected channels.

I built Kimberly Snyder from a $500 per hour private nutritionist into a multi-million dollar authority brand. I treated her presence as an asset structure, not a content schedule. 60 million pageviews. 150,000 email subscribers. Three New York Times bestsellers, including one co-authored with Deepak Chopra. The intangible asset was not her techniques.

It was the trust pattern stakeholders built across years of consistent voice, structured ideas, and visible judgment.

I map the full system in GURU, INC. The model applies the same way at the founder-CEO level. The asset is not the post. It is the compounding infrastructure behind the post.

The Founder Is the Most Mispriced Line on the Balance Sheet

The economy inverted while most boardrooms watched the wrong line. Buildings depreciated. Equipment got written down. Reputation, trust, and stakeholder confidence got reclassified as enterprise value. Most companies still treat the asset that produces them as a marketing line item.

If 92 percent of corporate value is intangible, the highest-leverage intangible inside any company is the founder. The voice that sets direction. The judgment investors price. The conviction acquirers pay multiples for. None of that lives in a logo, a deck, or a press release.

The trademark protects what was. The founder produces what comes next. One was the asset of the old economy. The other is the asset of this one.

Frequently Asked Questions

What does intangible asset mean in corporate finance?

Intangible assets are non-physical sources of business value, including brand recognition, intellectual property, stakeholder relationships, and reputation. Ocean Tomo classifies them as the dominant component of S&P 500 market value, now 92 percent as of 2025.

Is reputation measurable as a financial asset?

Yes. Burson's 2026 study modeled reputation across 66 publicly traded companies. The research isolated 4.78 percent in unexpected annual shareholder return tied to stakeholder perception. The methodology was validated at Oxford's Saïd Business School.

What is the difference between a corporate brand and a founder brand?

A corporate brand is an abstraction designed for narrow distribution channels and the tangible-heavy economy. A founder brand is a person whose judgment, voice, and visibility carry the trust signal directly to stakeholders. No logo is needed as intermediary.

How do international markets compare on intangible asset share?

The S&P Europe 350 holds intangible asset levels at 70 to 75 percent across volatile periods. Japan saw uplift after corporate governance reforms. China's CSI 300 declined after regulatory intervention in technology and education sectors.

Why is founder visibility considered an intangible asset?

Founder visibility produces concentrated trust among investors, acquirers, talent, and customers. That trust is a measurable input into valuation, deal terms, and hiring outcomes. By definition, that makes it an intangible asset.

Can a board treat founder visibility as a governable asset?

Yes. Boards already govern earnings communication, financial controls, and crisis response. Treating founder visibility with the same rigor formalizes an asset that already moves valuation. Governance does not mean controlling the founder's voice or scripting the message.